Equity Release Calculator

For a 65-year-old with a £300,000 property, you could potentially access up to £90,000 (30% of value).

For a 75-year-old, this could rise to up to £120,000 (40% of value).

Enter your details above and click Calculate to see your specific results.

Equity release lets homeowners over 55 unlock cash tied up in their property without selling or moving. But it’s not a simple loan. There are strict rules, hidden traps, and long-term consequences you need to understand before signing anything. If you’re considering it, here’s what actually matters - no fluff, just the facts.

Who Can Use Equity Release?

You must be at least 55 years old to qualify for any mainstream equity release product in the UK. Some providers raise the minimum age to 60, but 55 is the industry standard. Your home must be your main residence, and it needs to be worth at least £70,000. Most lenders won’t touch a property that’s a leasehold with under 75 years left, or one that’s in poor condition. If you’re still paying off your mortgage, you’ll need to clear it first - either with the release funds or your own savings.

Joint applications are allowed if both people are over 55. If one person is younger, the plan will be based only on the older person’s age. That means the younger partner might be forced to leave the home if the older one passes away. This catches many people off guard. Always check what happens if one partner dies or needs long-term care.

How Much Can You Release?

The amount you can access depends on your age, property value, and health. Generally, the older you are, the more you can borrow. Someone aged 65 might get around 30% of their home’s value. At 75, that jumps to 40% or more. Some lenders offer up to 50% for people with serious health conditions - this is called a enhanced equity release plan.

For example, if your home is worth £300,000 and you’re 70, you might qualify for £100,000 to £120,000. But don’t assume you’ll get the maximum. Lenders also look at your income, existing debts, and whether you have dependents. They want to make sure you can cover ongoing costs like property taxes and maintenance.

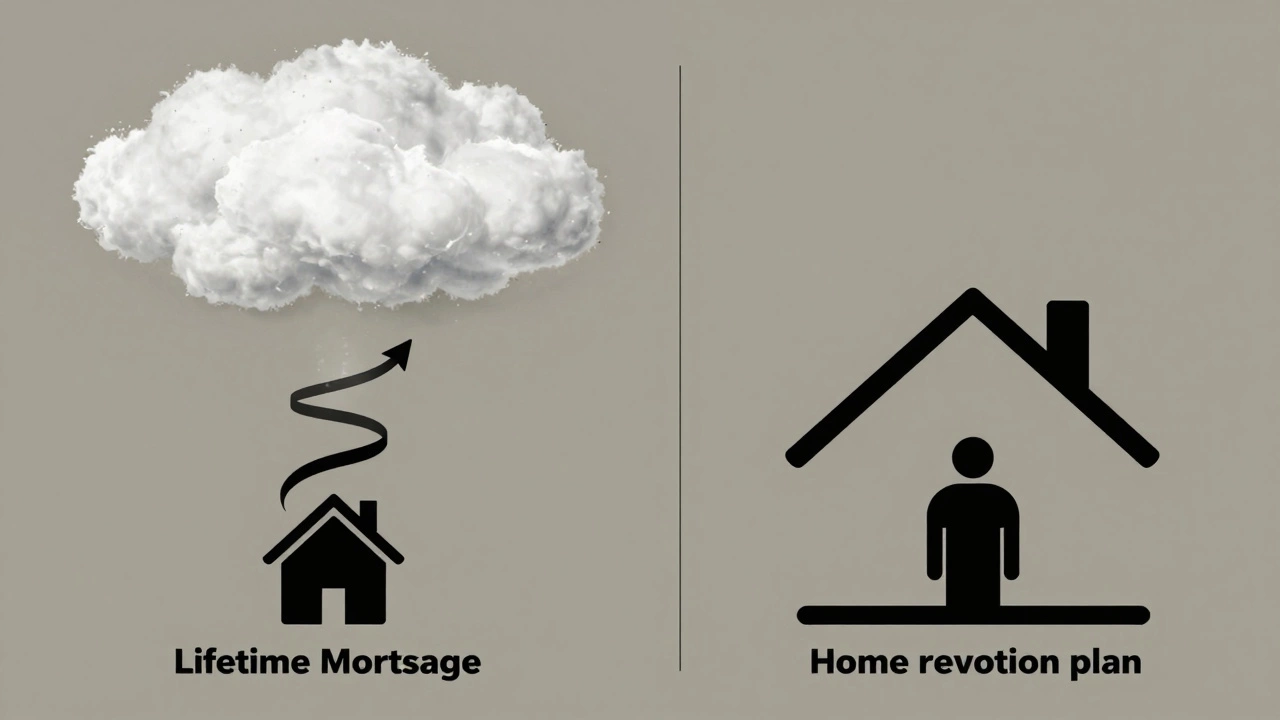

Two Main Types of Equity Release

There are only two legal structures for equity release in the UK: lifetime mortgages and home reversion plans. Most people choose the first.

- Lifetime mortgages: You take out a loan secured against your home. Interest rolls up over time. You keep full ownership and can live there for life. No monthly payments are required, but interest compounds - meaning what you owe can double or triple over 15-20 years.

- Home reversion plans: You sell part or all of your home to a provider in exchange for a lump sum or regular payments. You get to stay in the property rent-free, but you no longer own the portion you sold. If the home’s value rises, the provider keeps the profit.

Lifetime mortgages make up over 95% of the market. Home reversion plans are rare today because they offer less flexibility and worse value for most people.

Interest Rates and Costs

Interest rates on lifetime mortgages are fixed, but they’re much higher than standard mortgages. As of 2026, rates range from 5.8% to 7.5%. That’s two to three times higher than a typical 25-year mortgage. Why? Because lenders don’t get repaid until you die or move into care. They take on more risk - and charge for it.

On top of interest, you’ll pay setup fees: legal costs, valuation fees, advice fees, and arrangement fees. These can total £2,000 to £4,000. Some lenders offer fee-free deals, but they often make up for it with higher interest rates. Always compare the total cost over time, not just the upfront fee.

There’s also a no-negative-equity guarantee. This is mandatory by law. It means you’ll never owe more than your home’s value, even if interest builds up beyond that. If your estate is worth less than what you owe, your family won’t be left with a debt.

What Happens When You Die or Move?

When you pass away or move into long-term care, the property is sold. The proceeds pay off the loan - including all rolled-up interest - and any remaining money goes to your estate. If the sale doesn’t cover the full debt, the lender absorbs the loss thanks to the no-negative-equity guarantee.

But here’s the catch: if you’ve released £150,000 and interest has compounded to £300,000, your home might need to sell for £450,000 just to leave £150,000 for your heirs. If the market dips, your family could walk away with nothing. Many people don’t realize how fast interest adds up. A 6% rate over 20 years turns £100,000 into £320,000.

Can You Change Your Mind?

You can repay the loan early, but penalties apply. Most lenders charge an early repayment fee of 5% to 25%, depending on how long you’ve had the plan. If you repay within the first five years, you might pay 20% or more. After that, fees drop. Some newer plans offer penalty-free repayment after 10 years.

There’s also a cooling-off period of 14 days after signing. During that time, you can cancel without penalty. Use it wisely. Get a second opinion. Talk to your family. Don’t rush.

Impact on Benefits and Inheritance

Releasing equity can affect your eligibility for means-tested state benefits like Pension Credit, Council Tax Reduction, or help with care costs. If you take a large lump sum and keep it in the bank, it counts as savings. If you have over £20,000 in savings, you may lose some or all of your benefits.

It also reduces what you leave behind. If you planned to pass on your home to your children, equity release cuts into that. Some people use it to give money to family while they’re still alive - which can be a smart move if done right. But it’s irreversible. Once you sign, you can’t undo it.

What You Must Do Before Signing

By law, you must get advice from a FCA-regulated equity release adviser. They’re not allowed to push you toward a specific product. Their job is to explain all options and make sure it suits your situation. You’ll pay for this advice - usually £1,000 to £1,500 - but it’s worth every penny. Many people who regret equity release skipped this step.

Get at least two quotes. Ask for a detailed illustration showing how your debt grows over 10, 15, and 20 years. Compare the interest rate, fees, and early repayment terms. Ask: “What happens if I need care in five years?” and “Can I still move if I want to?”

Also, talk to your family. This isn’t just your decision. Your children might be counting on the property. If you don’t tell them, they’ll find out too late - and it could ruin relationships.

When Equity Release Makes Sense

It’s not for everyone. But it can be the right choice if:

- You need money to pay for home repairs, medical care, or help with living costs

- You don’t want to downsize or move

- You’ve already paid off your mortgage

- You’re not planning to leave a large inheritance

- You understand how compound interest works

If you’re still working, have other savings, or can cut expenses instead, equity release is probably not the best option. It’s a last-resort tool - not a lifestyle upgrade.

Common Mistakes to Avoid

- Signing without independent advice

- Choosing the highest lump sum without thinking about long-term interest

- Not telling your family

- Using the money for risky investments or gambling

- Assuming you can change your mind later without cost

One woman released £80,000 in 2018 to travel and help her grandchildren. By 2025, her debt had grown to £180,000. Her home sold for £200,000. Her children got £20,000 - less than she expected. She didn’t realize how fast interest added up.

Alternatives to Consider

Before choosing equity release, ask yourself:

- Can I downsize to a cheaper home and use the difference?

- Can I take out a standard mortgage or personal loan instead?

- Can I claim benefits I’m not currently receiving?

- Can I rent out a room under the Rent a Room Scheme?

- Is there a way to delay retirement or work part-time?

Downsizing often gives you more cash with no interest. A standard loan might cost less if you can afford repayments. Don’t default to equity release because it’s the most advertised option.

Can I still leave my home to my children if I use equity release?

Yes, but only if there’s money left after the loan is repaid. Because interest builds up over time, your home’s value may not cover the debt - especially if you release a large amount early. Many people end up with little or nothing to pass on. If inheritance is important to you, consider releasing only a small amount or choosing a plan with a drawdown option so you can control how much you borrow.

Do I have to make monthly payments with equity release?

No, you don’t have to make monthly payments on a lifetime mortgage. Interest is added to the loan balance each month and compounds over time. But you can choose to make voluntary payments - usually up to 10% of the original loan amount each year - to reduce the total debt. This can save you tens of thousands in interest over time.

What happens if I need long-term care?

If you move into long-term care, the equity release plan ends. Your home is sold, and the loan is repaid. If you’re part of a joint plan and your partner still lives in the home, they can stay until they die or decide to move. But if you’re the only borrower and you move out, the lender will start the process to sell the property.

Is equity release safe?

Yes, if you use a regulated provider and get independent advice. The no-negative-equity guarantee protects you from owing more than your home is worth. But safety doesn’t mean it’s right for everyone. It can reduce your inheritance, affect your benefits, and trap you in high-interest debt. It’s not risky because of fraud - it’s risky because of misunderstanding.

Can I still move house after taking out equity release?

Some plans allow you to transfer the loan to a new home - this is called portability. But not all do. If you think you might want to move, choose a plan that offers this feature. Otherwise, you’ll have to repay the full loan before moving, which can be difficult if you’ve already spent the money.