Debt Management: Simple Steps to Take Control of Your Finances

Feeling buried under multiple bills? You’re not alone. Most people juggle credit cards, personal loans, and maybe a student loan at the same time. The good news is that a clear plan can turn that chaos into manageable payments.

Why Debt Management Matters

When you ignore debt, interest keeps piling up and your credit score can take a hit. A lower score makes it harder to get a mortgage, a car loan, or even a rental agreement. By organizing your debt, you lower the total amount you’ll pay over time and protect your credit rating.

One of the fastest ways to tidy things up is a debt consolidation loan. It rolls several balances into one payment, often at a lower interest rate. But remember, not every loan is a win. Some consolidation options increase the overall cost or require you to put up collateral. Knowing the pros and cons helps you avoid hidden traps.

Top Strategies to Take Control

1. Check Your Credit Score First – Lenders usually want to see a score of 650 or higher for a consolidation loan. If you’re below that, focus on boosting your score by paying down high‑interest balances and fixing any errors on your credit report.

2. Know Which Debts Qualify – Most unsecured debt like credit‑card balances, medical bills, and personal loans can be combined. Secured debts such as a mortgage usually don’t qualify for standard consolidation programs.

3. Use the 50/30/20 Rule – Allocate 50% of your income to needs, 30% to wants, and 20% to savings or debt payoff. This simple budgeting method makes it easier to see where you can free up cash for extra payments.

4. Plan for Big Goals – Want to buy a house after consolidation? Lenders will look at your post‑consolidation credit profile. Keep your new loan on track, avoid new debt, and let your score recover before applying for a mortgage.

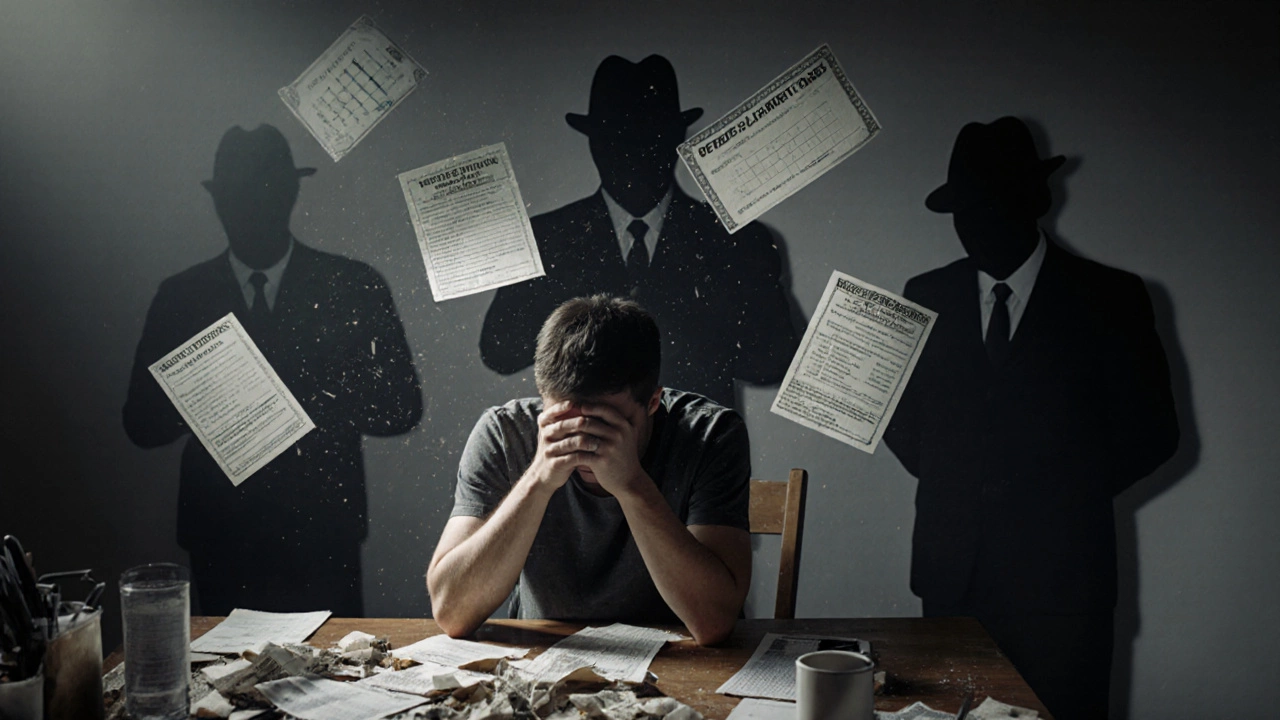

5. Watch Out for Scams – Some “national debt relief” companies promise quick fixes but charge huge fees or disappear with your money. Stick to reputable lenders, read reviews, and never pay upfront for a debt‑fix service.

If a consolidation loan isn’t an option, consider a debt management plan with a credit‑council. They negotiate lower interest rates with creditors and set up a single monthly payment. This can be a lifesaver when you’re denied a loan.

Finally, stay realistic about how fast you can pay off large balances. Cutting a $30,000 debt in a year is doable with a strict budget, extra income streams, and disciplined spending, but it requires sacrifice. Smaller goals, like paying off $5,000 in six months, build momentum and keep you motivated.

Remember, the goal isn’t just to eliminate debt—it’s to build habits that keep you financially healthy long after the last payment clears. Review your budget every month, keep an eye on your credit score, and adjust your plan as life changes. With these steps, you’ll turn debt from a constant worry into a manageable part of your financial story.

Learn what a zombie loan is and how to protect yourself from predatory debt buyers attempting to collect time-barred debts. Find out how to handle these requests safely.

Read More

Banks in Ireland do offer debt consolidation loans - usually as unsecured personal loans. Learn how they work, what you need to qualify, how rates compare, and how to avoid common mistakes that trap people in deeper debt.

Read More

Debt relief can hurt your credit, but not all types do. Debt settlement damages scores, while debt management plans and consolidation loans may help. Learn how each option affects your credit and how to recover.

Read More

Getting approved for debt consolidation depends on your credit score, income, and debt-to-income ratio. Learn what lenders look for and how to improve your chances-even with bad credit.

Read More

Debt consolidation doesn't erase bad credit. Late payments and settlements stay on your report for up to seven years. Learn how long it really takes to rebuild your score-and what to do after consolidation to make it faster.

Read More

If you never pay off your student loans, your credit will be damaged, wages garnished, and tax refunds seized. Default doesn’t disappear-it grows. Learn what really happens and how to fix it.

Read More

Discover how debt consolidation affects your credit score, the short‑term dip from hard inquiries, and proven steps to turn consolidation into a credit‑boosting move.

Read More

Wondering if a consolidation loan will hurt your credit score? Find out how these loans work, how they affect your credit, and tips to keep your score healthy.

Read More

Wondering what credit score you need to consolidate debt? Find out lender requirements, secret tips to qualify, and how to boost your odds fast.

Read More

Wondering if national debt relief companies are legit or just another scam? This article strips away the confusion around debt consolidation, explaining how real debt relief works, what to watch out for, and how you can protect yourself. You’ll find out how these programs operate, the warning signs of scams, and real steps for taking control of your debt. Consider this your no-nonsense guide to figuring out what’s real and what’s just empty promises.

Read More

Wondering if debt consolidation is the right move for you? This article breaks down how consolidating debts works, its real pros and cons, and how it might affect your financial life. You'll get practical advice, tips on what to look out for, and facts that can help you decide. No jargon—just real-life guidance you can use. Get answers to common questions and learn what to expect before jumping in.

Read More

Wondering if you can buy a house after consolidating your debt? This article breaks down what actually happens to your home-buying plans after debt consolidation, how your credit score is affected, and what lenders look for. Get real tips on improving your chances, common mistakes to avoid, and how timing can make a big difference for your mortgage approval. A practical guide for anyone who wants a fresh start without sacrificing their dream home.

Read More