Imagine opening your mail to find a letter from a company you've never heard of, claiming you owe them €2,000 from a credit card you closed a decade ago. You remember the debt, but you also remember that it was settled or simply disappeared from your radar years ago. This is the classic setup for a zombie loan. It isn't a real monster, but it behaves like one-it's a debt that was effectively dead, only to be brought back to life by a debt buyer who hopes you'll pay up without checking the rules.

Quick Facts About Zombie Debt

- Legal Status: Often time-barred, meaning the creditor cannot successfully sue you for the money.

- The Trap: Making a small payment or acknowledging the debt in writing can "restart the clock."

- Common Sources: Old credit cards, forgotten personal loans, or medical bills.

- The Goal: Debt buyers purchase these portfolios for pennies on the euro and hope for a quick settlement.

How the "Resurrection" Process Works

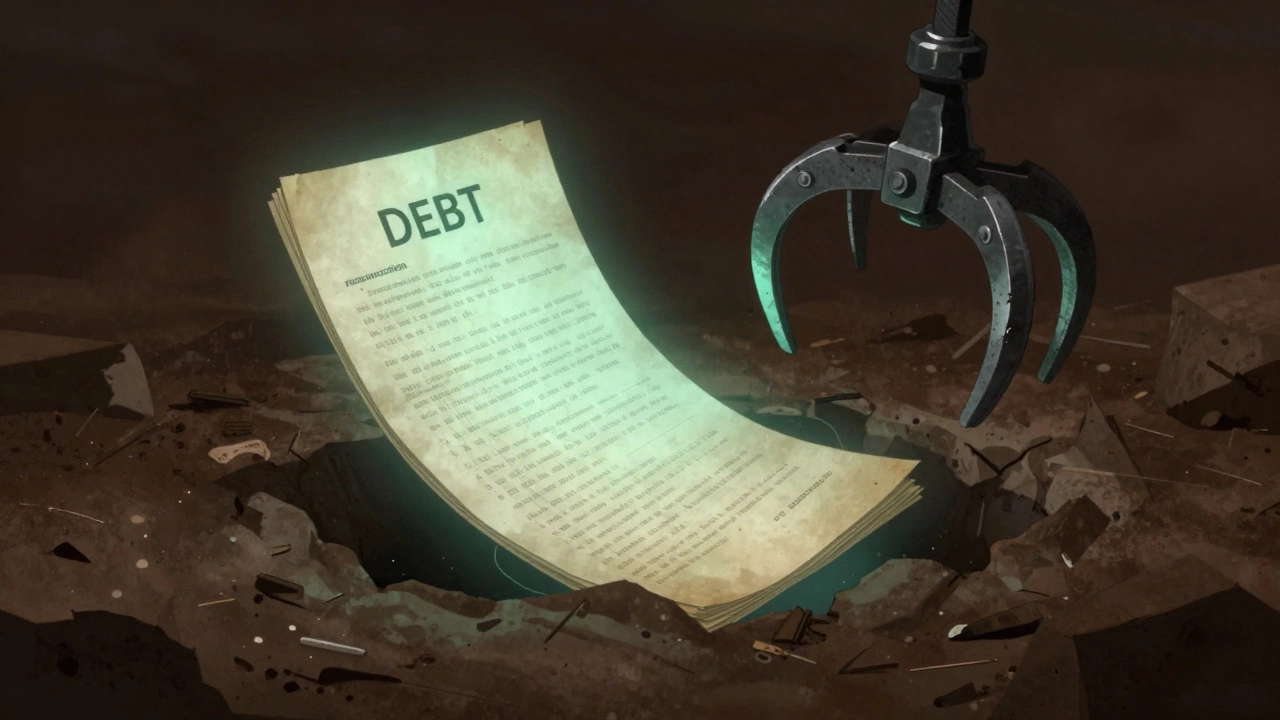

To understand why these loans appear, you have to look at the secondary debt market. When a bank or lender decides a loan is uncollectible, they don't just delete the record. Instead, they sell the debt to Debt Buyers-specialized firms that buy thousands of delinquent accounts in bulk. These buyers don't care if the debt is ten years old; they only care that the data exists.

The process usually follows a specific pattern. First, you get a vague letter or a phone call. The tone is often urgent, threatening legal action or a hit to your credit score. They rely on fear. If you panic and pay just €10 to "show good faith," you have just performed a legal miracle: you've acknowledged the debt, which in many jurisdictions resets the Statute of Limitations. This gives the zombie loan a new lease on life, making it legally enforceable again.

The Legal Shield: The Statute of Limitations

The only thing keeping zombie loans in the grave is the law. Every region has a limit on how long a creditor has to take you to court. For example, in many places, if a creditor hasn't contacted you or you haven't made a payment for six years, the debt becomes "time-barred." This doesn't mean the debt vanishes-you still technically owe it-but it means the court will throw out any lawsuit the collector tries to file.

The trick is that debt collectors rarely tell you a debt is time-barred. Why would they? If you knew the law, you'd ignore the letter. They want you to believe that the legal window is still open. If you are dealing with a loan from 2012 and it's now 2026, the odds are high that the legal window has slammed shut.

| Feature | Active Loan/Debt | Zombie Loan (Time-Barred) |

|---|---|---|

| Legal Enforceability | Can lead to court judgments | Generally cannot be enforced in court |

| Ownership | Original Lender (Bank) | Third-party Debt Buyer |

| Communication | Regular statements/reminders | Sudden, aggressive contact after years |

| Risk of Payment | Required to avoid default | Payment may accidentally restart legal clock |

Red Flags That You're Being Targeted

Not every old debt is a zombie loan, but there are certain patterns that should make you suspicious. If you receive a notice that doesn't list the original creditor's name or the exact date of the last payment, be careful. Real banks have meticulous records; zombie debt buyers often have messy spreadsheets with missing data.

Another red flag is the "limited time offer." They might tell you that if you pay 50% of the balance today, they'll wipe the rest. This is a common tactic to get you to make a payment. Once that money hits their account, they have proof of payment and a fresh legal claim to come after you for the remaining 50%.

Steps to Handle a Zombie Loan Request

If you suspect a debt is time-barred, the worst thing you can do is call them and start negotiating. Instead, follow a strict protocol to protect your finances.

- Stay Silent: Do not admit the debt is yours over the phone. Do not promise to pay "something" next week.

- Demand Verification: Send a written request (via registered post) asking for a "Debt Validation Letter." This forces them to provide the original contract and a full history of the debt.

- Check the Dates: Once you have the validation letter, look for the date of the last payment. Compare this to your local statute of limitations.

- Send a "Cease and Desist": If the debt is time-barred, write back stating that the debt is statute-barred and that they must stop contacting you.

- Monitor Your Credit: Use a credit reporting agency to ensure the buyer hasn't added a fraudulent entry to your report to pressure you.

The Psychological Trap of Debt Guilt

Debt buyers don't just use legal loopholes; they use psychology. Many people feel a deep moral obligation to pay back money they borrowed, even if the legal time has passed. They play on this guilt. However, you have to distinguish between a moral obligation and a legal one.

In a world where Debt Management is so complex, protecting yourself from predatory buyers is a form of financial self-defense. If a company bought your debt for 1% of its value, they aren't acting out of a sense of justice; they are running a high-profit business based on catching people who don't know their rights.

Dealing with Aggressive Collection Tactics

Some agencies go beyond letters and start harrassing your neighbors or calling your workplace. In most developed countries, there are strict laws governing how collectors can behave. If they are calling you ten times a day or threatening you with jail time-which is almost never the case for civil debt-they are likely violating consumer protection laws.

Keep a log of every interaction. Save every email and record the time of every call. If the harassment continues after you've told them the debt is time-barred, you may have grounds to file a complaint with a financial regulator or ombudsman.

Can a zombie loan affect my credit score?

Generally, most credit reporting agencies remove debts from your report after a certain period (often 6-7 years). If the debt is truly a "zombie" and has been off your report for years, a debt collector cannot simply put it back on. However, if you make a payment or acknowledge the debt, some collectors may try to report the account as "updated" or "active," which could potentially damage your score.

What happens if I just ignore the letters?

Ignoring them is often a safe bet if you are certain the debt is time-barred, but it can be stressful. The better approach is to send a single, formal letter stating that the debt is statute-barred and requesting they cease all communication. This creates a paper trail that you can use in court if they decide to sue you anyway, allowing your lawyer to get the case dismissed quickly.

Is it illegal for them to try to collect a zombie loan?

It is not necessarily illegal to ask for payment of a time-barred debt, but it is illegal to mislead you into thinking they can take legal action if they cannot. If a collector claims they will sue you in court for a debt they know is statute-barred, they may be committing a regulatory violation or fraud, depending on your local laws.

Does paying a small amount reset the clock?

Yes. This is the biggest danger of zombie loans. In many jurisdictions, any payment-even €1-is seen as an acknowledgment of the debt. This "re-ages" the debt and restarts the statute of limitations timer from zero, giving the collector a brand new window to sue you for the full amount.

How do I know if my debt is officially "time-barred"?

You need to find the date of your last payment or the last time you acknowledged the debt in writing. Check your old bank statements if possible. Then, check the laws in your specific state or country. If that time gap exceeds the legal limit (e.g., 6 years in many UK/Irish contexts or varying years in US states), the debt is likely time-barred.