Remortgage Equity Calculator

Calculate your current equity percentage to see if you qualify for remortgaging in Ireland. Most lenders require at least 20% equity (80% LTV).

Your Equity Analysis

Lenders' Perspective

Most Irish lenders require at least 20% equity (80% LTV) for remortgaging. Some may accept up to 85% LTV with excellent credit, but this is rare.

When you think about remortgaging, you’re probably imagining a lower interest rate, a bigger loan, or cash out for home improvements. But here’s the real question most people miss: how much equity do you actually need to make it work?

In Ireland, equity isn’t just a number on a spreadsheet-it’s your bargaining chip. The more you have, the better your deals. The less, the more you’ll struggle to get approved. And it’s not just about what you think your house is worth. Banks use strict rules, and they don’t bend.

What Is Equity, Really?

Equity is the part of your home you truly own. It’s not your mortgage balance. It’s not your purchase price. It’s the difference between what your house is worth right now and how much you still owe.

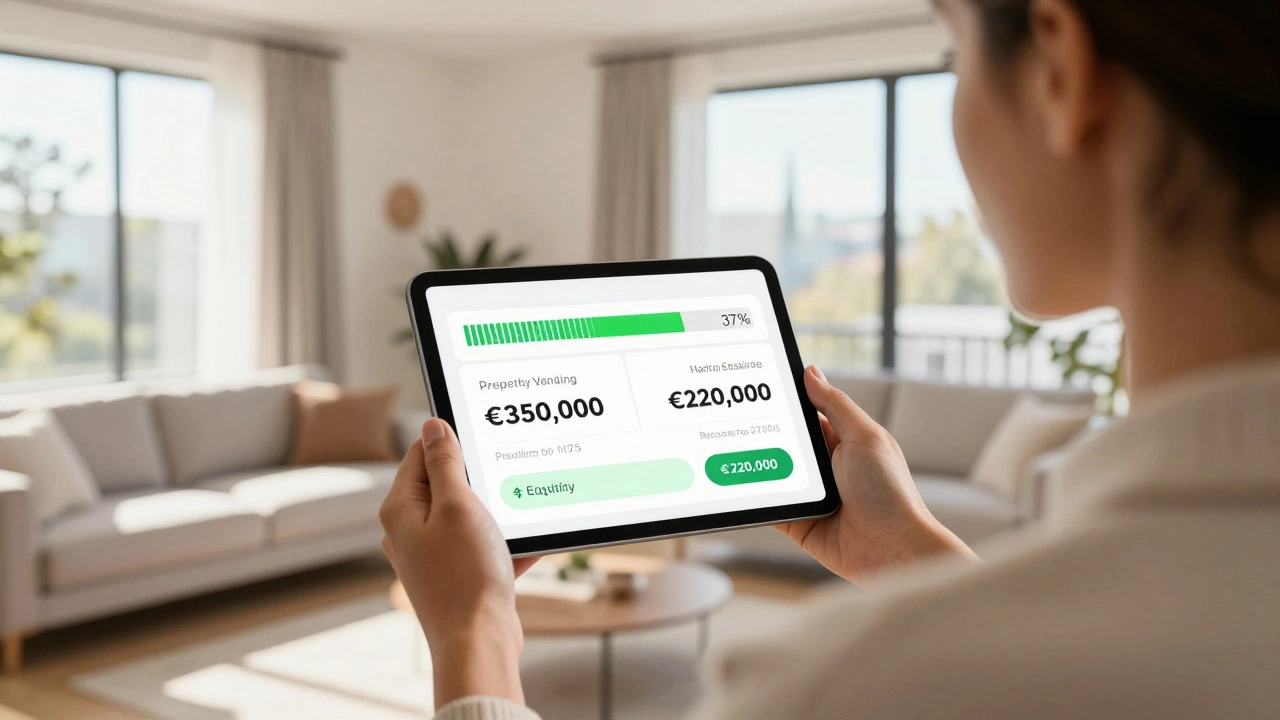

Let’s say you bought a house for €300,000. You put down €60,000 and borrowed €240,000. Two years later, your home is worth €350,000. You’ve paid off €20,000 of your mortgage. So your current loan balance is €220,000.

Your equity? €350,000 minus €220,000 = €130,000.

That’s over a third of your home’s value. And that’s what lenders look at.

The Minimum Equity You Need

Most Irish banks won’t let you remortgage if your loan-to-value (LTV) ratio is above 80%. That means you need at least 20% equity.

Let’s break that down:

- If your home is worth €350,000, 80% LTV means you can borrow up to €280,000.

- If you still owe €220,000, you’re at 63% LTV-well under the limit. You’re in a strong position.

- If you owe €290,000, you’re at 83% LTV. That’s over the line. Most lenders will say no.

Some lenders might stretch to 85% LTV if you have excellent credit, a high income, or are switching from another lender with them. But that’s rare. Don’t count on it.

Bottom line: 20% equity is the safe minimum. Anything below that makes remortgaging extremely difficult.

Why Does Equity Matter So Much?

Banks aren’t being picky just to be annoying. They’re protecting themselves.

If you default on your mortgage, they sell your house to get their money back. If the house sells for less than what you owe, they lose money. That’s why they need a buffer.

That buffer? Your equity.

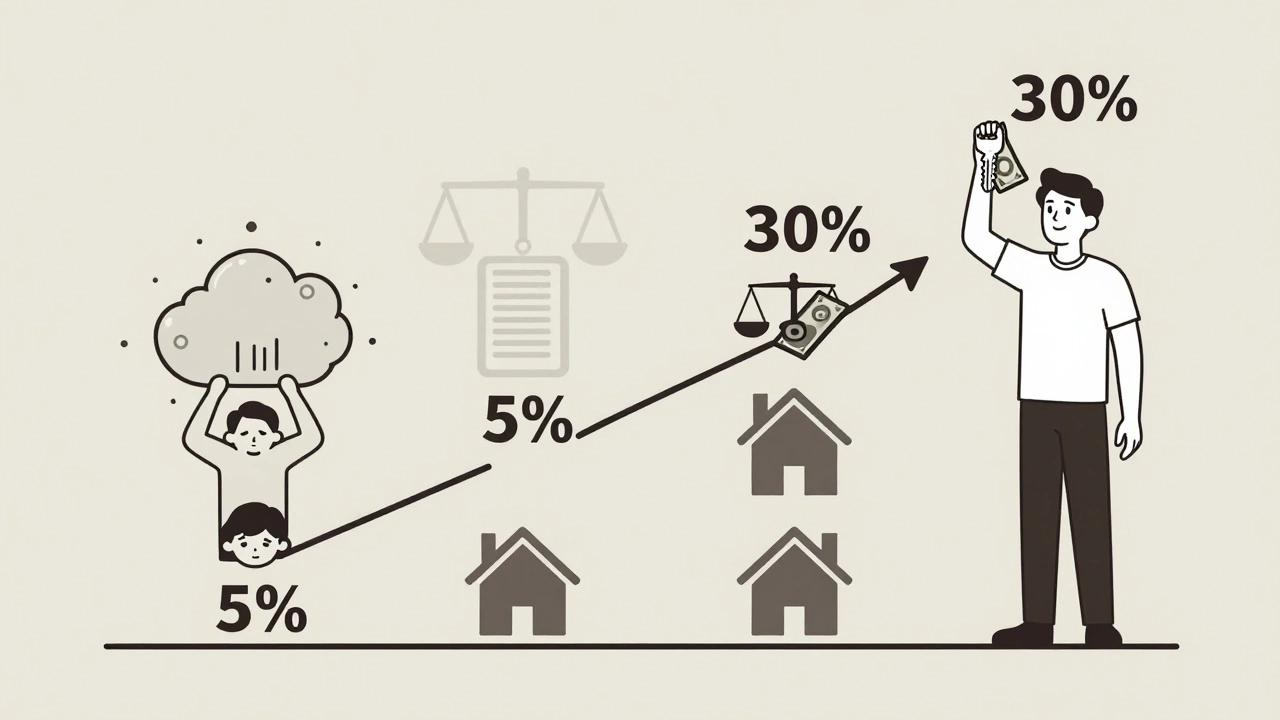

With 20% equity, even if house prices drop 10%, you still have a cushion. If you have only 5% equity and prices fall 10%, you’re underwater. And lenders hate underwater mortgages.

Also, higher equity = better rates. You’re seen as low-risk. That means:

- Lower interest rates

- Better terms

- More lenders willing to offer you a deal

One client I worked with had €180,000 equity on a €400,000 home. She got a fixed rate of 2.9% for five years. Her neighbour, with only €50,000 equity, was offered 4.1%-and only if they added a €2,500 arrangement fee.

Can You Remortgage with Less Than 20% Equity?

Technically, yes. But it’s messy.

Some specialist lenders offer up to 90% LTV, but they come with strings:

- Higher interest rates (often 0.5%-1.5% more)

- Strict income checks (you need to earn 4-5x the mortgage amount)

- Extra fees (valuation fees, legal fees, arrangement fees)

- Only available if you’re switching lenders within the same bank group

And even then, you’ll likely need a strong credit score (750+), no missed payments in the last 24 months, and proof of stable income.

Most people who try to remortgage with under 15% equity end up stuck. They get rejected, waste time, and damage their credit file with too many applications.

How to Check Your Equity

You can’t guess this. You need numbers.

Here’s how to find out:

- Get a current valuation. Use Daft.ie or MyHome.ie to compare similar homes in your area. Look at recent sales (last 3-6 months), not asking prices.

- Call your current lender. They’ll tell you your exact outstanding balance.

- Subtract your balance from your estimated value. That’s your equity.

Example: Your home is valued at €380,000. You owe €290,000. Equity = €90,000. That’s 23.7% equity. You’re in a good position.

Pro tip: Don’t rely on your original valuation. House prices in Dublin rose 18% between 2022 and 2025. If you bought in 2020, your equity is probably higher than you think.

What If You Want to Cash Out?

Many people remortgage to take money out-pay for renovations, help family, or invest.

But here’s the catch: lenders don’t let you borrow up to 80% of your home’s value and take cash out. They cap the total amount you can borrow.

Let’s say your home is worth €400,000. You owe €200,000. You have €200,000 equity.

You want €50,000 cash out. That means you’d need a new mortgage of €250,000.

€250,000 divided by €400,000 = 62.5% LTV. That’s fine. You’re well under the 80% limit.

But if you owed €300,000 and wanted €50,000 cash, you’d need a €350,000 mortgage. €350,000 / €400,000 = 87.5% LTV. That’s over the limit. No deal.

So if you want cash out, you need extra equity to cover it. No exceptions.

What Else Matters Besides Equity?

Equity is the gatekeeper. But once you’re in, other things decide if you get the best deal:

- Income stability - Are you on a permanent contract? Self-employed? Lenders want proof of income over the last 2 years.

- Credit score - A score below 700 makes approval harder. Missed payments? You’ll need to explain them.

- Debt-to-income ratio - If you have car loans, credit cards, or personal loans, your monthly payments count. Lenders don’t want you spending more than 35-40% of your income on debt.

- Property type - Detached houses are easiest. Apartments in high-rise buildings? Some lenders avoid them.

One woman in Bray had 30% equity but a credit score of 660 because she missed two payments during a job loss. She got approved-but only with a 4.8% rate and a €3,000 fee. She waited six months, rebuilt her credit, then remortgaged again and got 3.1%.

When Not to Remortgage

Just because you can doesn’t mean you should.

Don’t remortgage if:

- You’re within the first year of a fixed rate-you’ll pay early repayment charges (often 2-5% of the loan)

- You’re planning to move in the next 2 years

- Your income is unstable or you’re about to change jobs

- You’re using the cash for non-essential spending (holidays, new cars)

Remortgaging isn’t a magic fix. It’s a financial tool. Use it to save money, not spend it.

Next Steps

Here’s what to do next:

- Check your current mortgage balance with your lender.

- Get a free valuation from Daft.ie or MyHome.ie.

- Calculate your equity: (Current value - Outstanding balance).

- If it’s above 20%, start comparing rates. Use Moneyfacts.ie or your broker.

- If it’s below 20%, focus on paying down your mortgage first. Even €5,000 extra a year can get you over the line in 3-4 years.

Don’t rush. The best deals don’t come from panic. They come from preparation.