Mortgage Affordability Calculator

Loan Details

Additional Costs

Estimated Monthly Breakdown

To keep this under 28% of gross income, you need a monthly salary of at least $0.

That number in your head is probably wrong. Most people guess their monthly mortgage payment by dividing the loan amount by 360 months and ignoring interest entirely. If you borrow $150,000 is a common mid-range home purchase price or refinance amount that requires careful calculation of principal, interest, taxes, and insurance to determine true affordability, you aren’t just paying back that cash. You’re paying for the privilege of borrowing it over time.

In mid-2026, with average interest rates hovering around 6.5% to 7.5% for conventional loans, the reality of what you owe each month can shock first-time buyers and surprise those looking to remortgage. This isn't just about math; it's about understanding where your money goes so you don't get blindsided by hidden costs like property taxes or private mortgage insurance (PMI).

The Base Payment: Principal and Interest Only

Let’s strip away the extras for a second. The core of your mortgage is the Principal and Interest (P&I) is the foundational component of a mortgage payment that repays the borrowed amount plus the cost of borrowing over the loan term. This is the money going directly to your lender.

If you take out a standard 30-year fixed-rate mortgage at a 7.0% interest rate-which is a realistic benchmark for 2026-your monthly P&I payment would be approximately $998. That’s nearly $1,000 every single month for three decades. But here’s the kicker: if you opt for a 15-year term to save on interest, that same $150,000 loan at 6.5% jumps to roughly $1,294 per month. You pay off the debt faster, but your monthly cash flow takes a hit.

Why does the term matter so much? Because with a 30-year loan, you spend the first several years paying mostly interest. In the first year alone, less than 10% of your payment goes toward reducing the actual loan balance. With a 15-year loan, you chip away at the principal much quicker, which builds equity faster but demands higher immediate income stability.

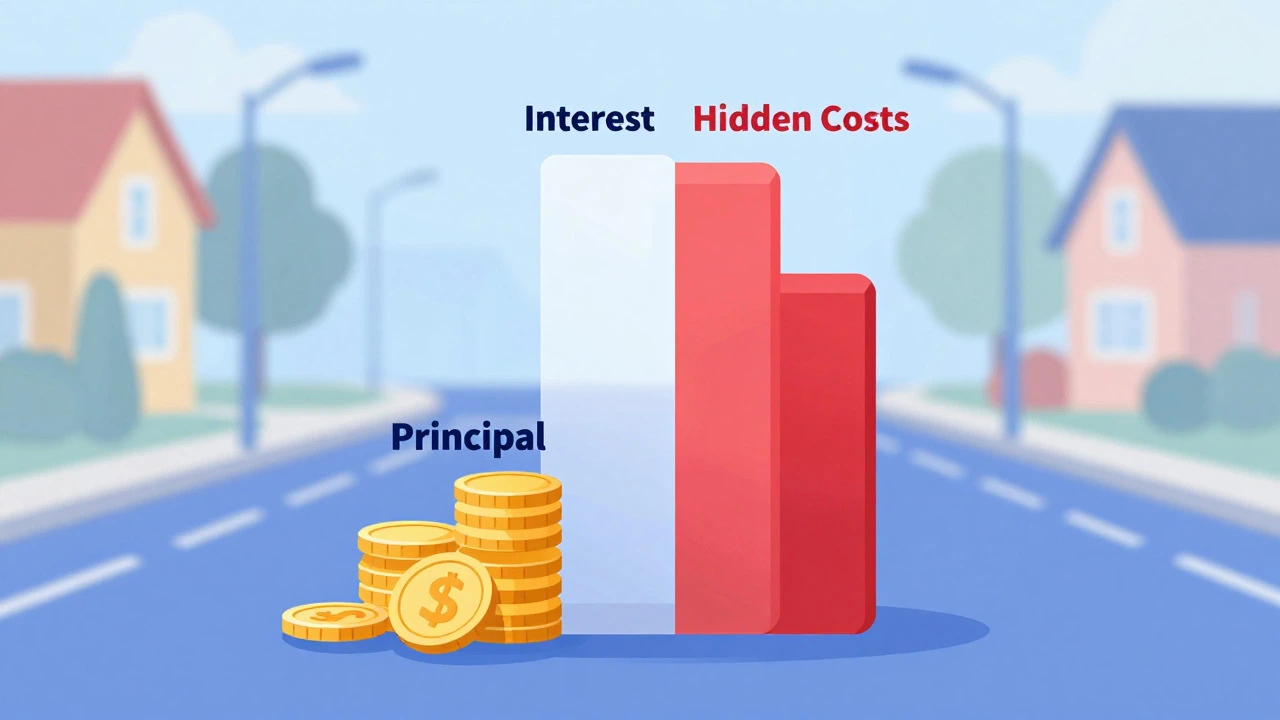

The Hidden Costs: Taxes, Insurance, and PMI

Your bank statement won’t just show $998. It will likely show more. Lenders often require an Escrow Account is a separate account managed by the lender used to collect and pay property taxes and homeowners insurance premiums on behalf of the borrower. This means your "total monthly payment" includes estimates for property taxes and homeowners insurance.

- Property Taxes: These vary wildly by location. In a high-tax state like New Jersey or Illinois, taxes might run 2% to 3% of the home’s value annually. On a $150,000 assessment, that’s $3,000 to $4,500 a year, or $250 to $375 a month. In lower-tax areas like Texas or Hawaii, it could be under $100 a month.

- Homeowners Insurance: A standard policy might cost $1,200 to $1,500 annually, adding another $100 to $125 to your monthly bill.

- Private Mortgage Insurance (PMI): If you put down less than 20%, you’ll pay PMI. For a $150,000 loan with a 5% down payment ($7,500), your loan amount is actually $142,500, but let’s stick to the $150k base for simplicity. PMI typically costs 0.5% to 1% of the loan amount annually. That’s an extra $62 to $125 per month until you reach 20% equity.

Add these up, and your "real" monthly payment could easily range from $1,200 to $1,600 depending on where you live and how much you put down. Ignoring these components is the fastest way to overextend your budget.

How Interest Rates Change Your Reality

Interest rates are not static. They fluctuate based on Federal Reserve policies, inflation data, and economic health. In 2026, we’ve seen rates stabilize after the volatility of previous years, but they remain higher than the historic lows of the early 2020s.

| Interest Rate | Monthly P&I Payment | Total Interest Paid Over Life of Loan |

|---|---|---|

| 5.5% | $861 | $159,960 |

| 6.0% | $900 | $173,990 |

| 6.5% | $948 | $191,280 |

| 7.0% | $998 | $209,280 |

| 7.5% | $1,050 | $228,000 |

Notice the jump? Moving from a 6.0% rate to 7.0% adds nearly $100 to your monthly payment and over $35,000 to the total cost of the house. This is why locking in a rate matters. Even a small fraction of a percent can mean thousands of dollars in savings-or loss.

Remortgaging: Is It Worth It in 2026?

You mentioned Remortgaging is the process of replacing an existing mortgage with a new one, often to secure a lower interest rate, switch loan terms, or access equity. Many homeowners are asking if now is the right time to refinance their $150,000 mortgages. The answer depends on your current rate versus today’s market.

If you locked in a rate below 5% during the pandemic era, refinancing at 7% would be a financial disaster. Your payments would skyrocket. However, if you have an adjustable-rate mortgage (ARM) that has reset to a painful level, or if you originally took out a subprime loan with a high rate, refinancing into a conventional fixed-rate loan could save you money.

Consider the break-even point. Refinancing costs money-closing fees, appraisal fees, title insurance. These typically run 2% to 5% of the loan amount. On $150,000, that’s $3,000 to $7,500 upfront. If your monthly savings are $100, it will take you 30 to 75 months to recoup those costs. Do you plan to stay in the home that long? If not, refinancing might not make sense.

Strategies to Lower Your Monthly Payment

You don’t have to accept the highest possible payment. There are levers you can pull to reduce the burden on your monthly budget.

- Put Down More Than 20%: This eliminates PMI entirely. If you can scrape together an extra $10,000 for your down payment, you might save $100+ a month in insurance premiums.

- Choose a 20-Year Term: It’s a middle ground between 15 and 30 years. You’ll pay less interest than a 30-year loan but have lower monthly payments than a 15-year loan.

- Shop Around for Lenders: Don’t just go to the big bank. Credit unions and online lenders often offer better rates for borrowers with good credit scores (740+). Getting multiple quotes can shave 0.25% off your rate, saving you hundreds over the life of the loan.

- Consider Discount Points: You can pay upfront fees (points) to buy down your interest rate. One point costs 1% of the loan amount ($1,500) and might lower your rate by 0.25%. Calculate the break-even period carefully.

What About Adjustable-Rate Mortgages (ARMs)?

An Adjustable-Rate Mortgage (ARM) is a mortgage with an interest rate that changes periodically based on market conditions, offering lower initial rates but higher long-term risk might look tempting because the starting rate is often 0.5% to 1% lower than a fixed-rate loan. For a $150,000 loan, a 5/1 ARM might start at 6.0% instead of 7.0%.

That saves you about $50 a month initially. But after five years, the rate adjusts. If rates rise further, your payment could jump significantly. ARMs are risky in a rising rate environment like 2026. They’re best suited for people who plan to sell or refinance within the initial fixed period. If you’re staying put long-term, the uncertainty usually isn’t worth the short-term savings.

Bottom Line: Budget for the Worst Case

When calculating whether you can afford a $150,000 mortgage, never budget for the lowest possible payment. Budget for the highest likely scenario. Include taxes, insurance, PMI, and a buffer for maintenance. A safe rule of thumb is that your total housing costs should not exceed 28% of your gross monthly income.

If your gross income is $6,000 a month, your max housing budget is $1,680. After accounting for P&I, taxes, and insurance, you’ll see if that $150,000 loan fits. If it doesn’t, you might need to increase your down payment, look for a cheaper home, or improve your credit score to qualify for a lower rate. Knowledge is power, and knowing exactly what those monthly numbers mean protects you from making a mistake that lasts thirty years.